{kind=link}

The increase in double application technology-infestation in each civil and military applications-quickly transforms the global landscape of technology. Once a area of interest, largely avoided as a result of LP restrictions in defense investments, the category is now front and center for governments, VC and startups.

Drivers are clear: intensifying geopolitical tensions, balloon defense budgets NATO Countries and the growing awareness that critical future possibilities of supervision based on AI to autonomous and protected communication systems shall be increasingly coming from traditional defense performers, but from agile, highly developing startups.

How big is the double application technology? How much does defense cost?

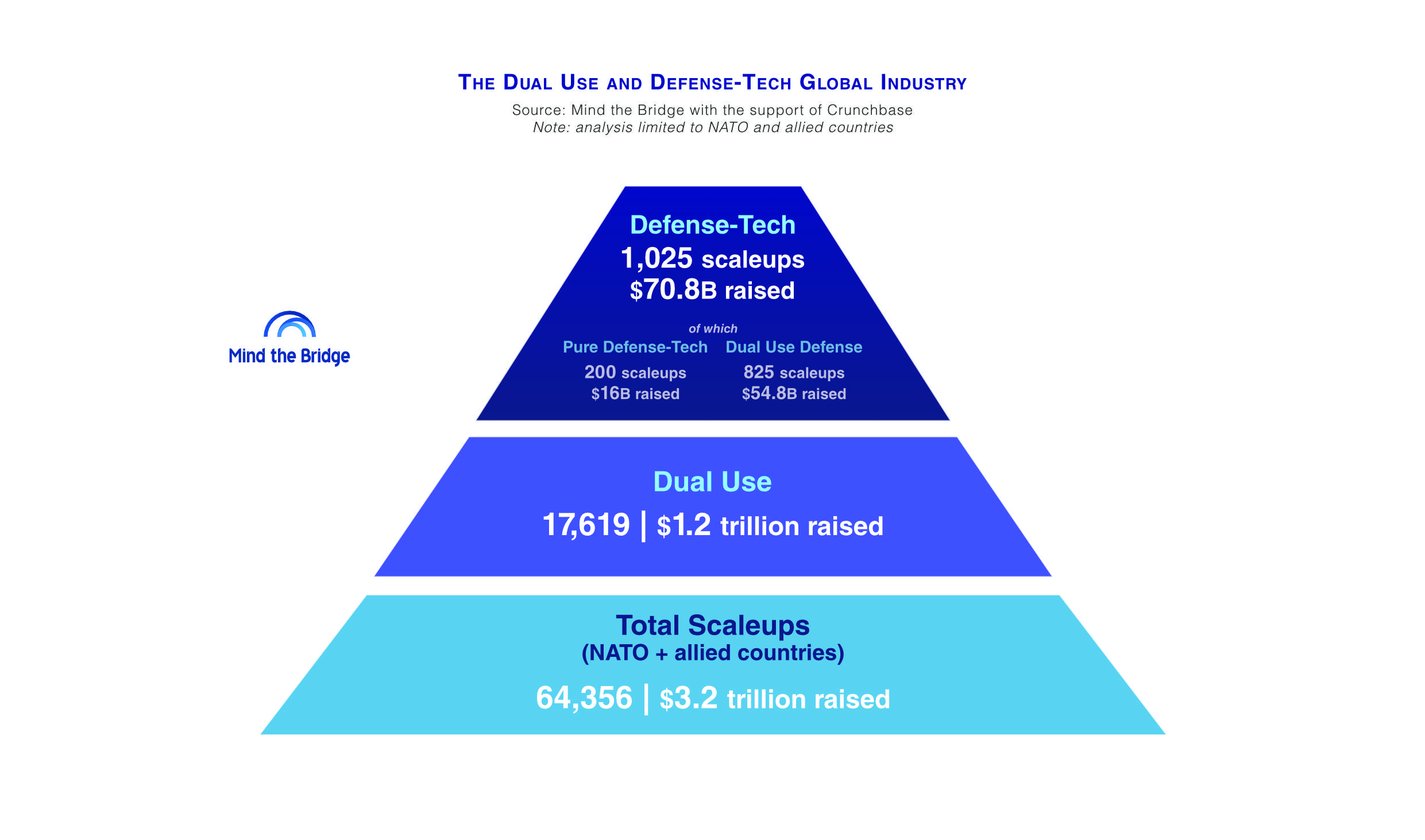

Since May 2025, NATO has been operating in NATO countries 17,619 of the scale of double use technology-among around 64,000 scale identified in 47 analyzed countries.

In this cohort:

- 1025 is divided on a scale of defense technologies.

- Of these, 200 are “pure defense technologies” or startups focusing only on military applications.

- The remaining 825 is the “double-application defense technology”-stations, which began with civil technologies and later evolved, including defense-oriented solutions.

In other words, the technical scale of double application currently constitute 27% of the total scale population in the surveyed countries. This is 1 on 4 scales developing technologies with potential military or defensive applications.

Increase in double use technology

This is not a trend anymore – this is a sharp growth. Powered by fincantieri, Watch out for the bridge and Crunchbase conducted the first evaluation at the end of 2024 (report Here). In half of 2025, we updated it (download Here) To reflect the latest achievements.

We discovered that in just six to eight months the growth was explosive.

- The number of scale of double application technology increased from 15 260 to 17 619, which is an increase of 16%.

- The scale of defense technology exceeded 1000 characters (increase of 13%), with pure defense technology grew even faster at 18%-a plus.

- The investment in double application technology increased by 25%, from 954.5 billion dollars in $ 3,2024 to almost $ 1.2 trillion in May 2025.

- The investment specific for defense technology increased by 27%, reaching $ 70.8 billion.

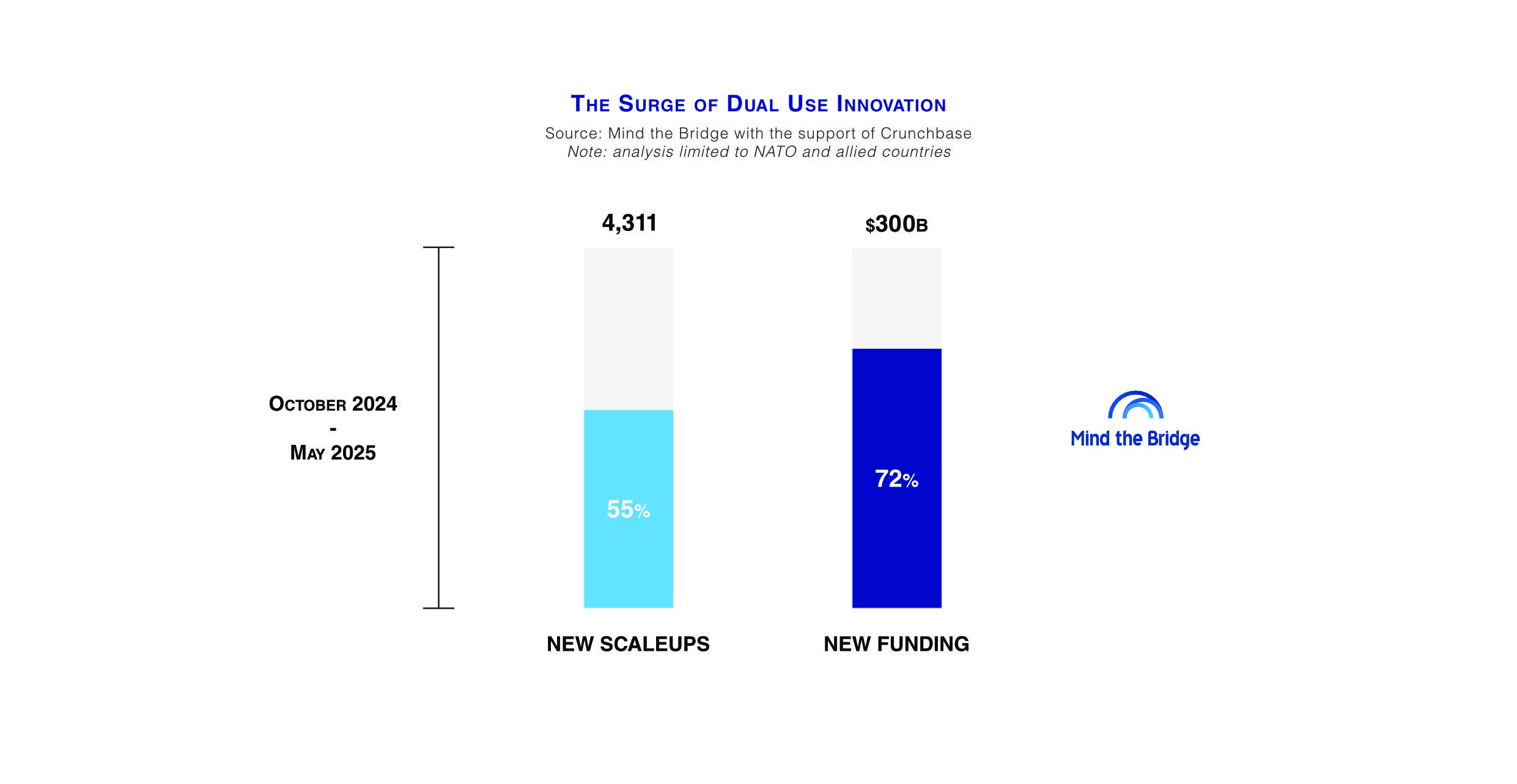

Only between October 2024 and May 2025:

- 4311 recent scale was created in NATO and related countries.

- Over half (2359) are technology firms with double use.

- About 70% of all recent investments on a scale during this era went to technological startups with a double application.

Where double use technology is more advanced

Israel was a pioneer of the model, transforming military research and development into technological power led by a startup. The US is following the growing network of integration programs (DiuIN AfwverxIN Hes) for on -board industrial innovations in the defense ecosystem.

Europe is catching up. Only in 2024 European Defense Fund. Meanwhile, national programs are expanding:

- Great Britain promised 400 million kilos for defensive innovations;

- Germany doubled the budget for military orders; AND

- The NATO Innovative Fund in the amount of EUR 1 billion began to support startups with double use in the alliance.

Even smaller, digitally advanced countries move quickly. Estonia is distinguished by the integration of the startup ecosystem with the National Defense Strategy. But this is not the same: Ukraine, Poland, Czech Republic and other Eastern European countries also invest in innovations in defense.

There are barriers

Despite this momentum, the innovations of double applications still face serious challenges. These startups develop hard technology with critical military applications – often requiring long research and development cycles and large rounds of financing.

Our data show that defense technological startups are more demanding. On average, $ 80 million collected on average. Compared to an average of $ 66 million for double application technology and $ 50 million for purely civil technology scale.

They also change into longer on the market, as a result of the bottlenecks and outdated acquisition models. This creates the notorious phase of the “Death Valley”.

Common barriers include:

- The fragility of the startup raises real concerns about survival;

- Many armed forces are not used to work with 6-speed TRL startups; AND

- The scaling and implementation of the field remain the foremost bottleneck. Defense startups cannot go alone. Most lack infrastructure for scaling of equipment production.

What’s more, startups with double use often suffer from the team “not here or there”-the plants between two demanding markets, without a full commitment to one of them. This can dilute the strategic concentration and increase in stretching.

Collecting funds and outputs are one other friction point:

- Many institutional LP stays undecided or hindered before defense -related projects.

- The output options are limited. Restrictions of national security often block foreign mergers and acquisitions, while local buyers are few.

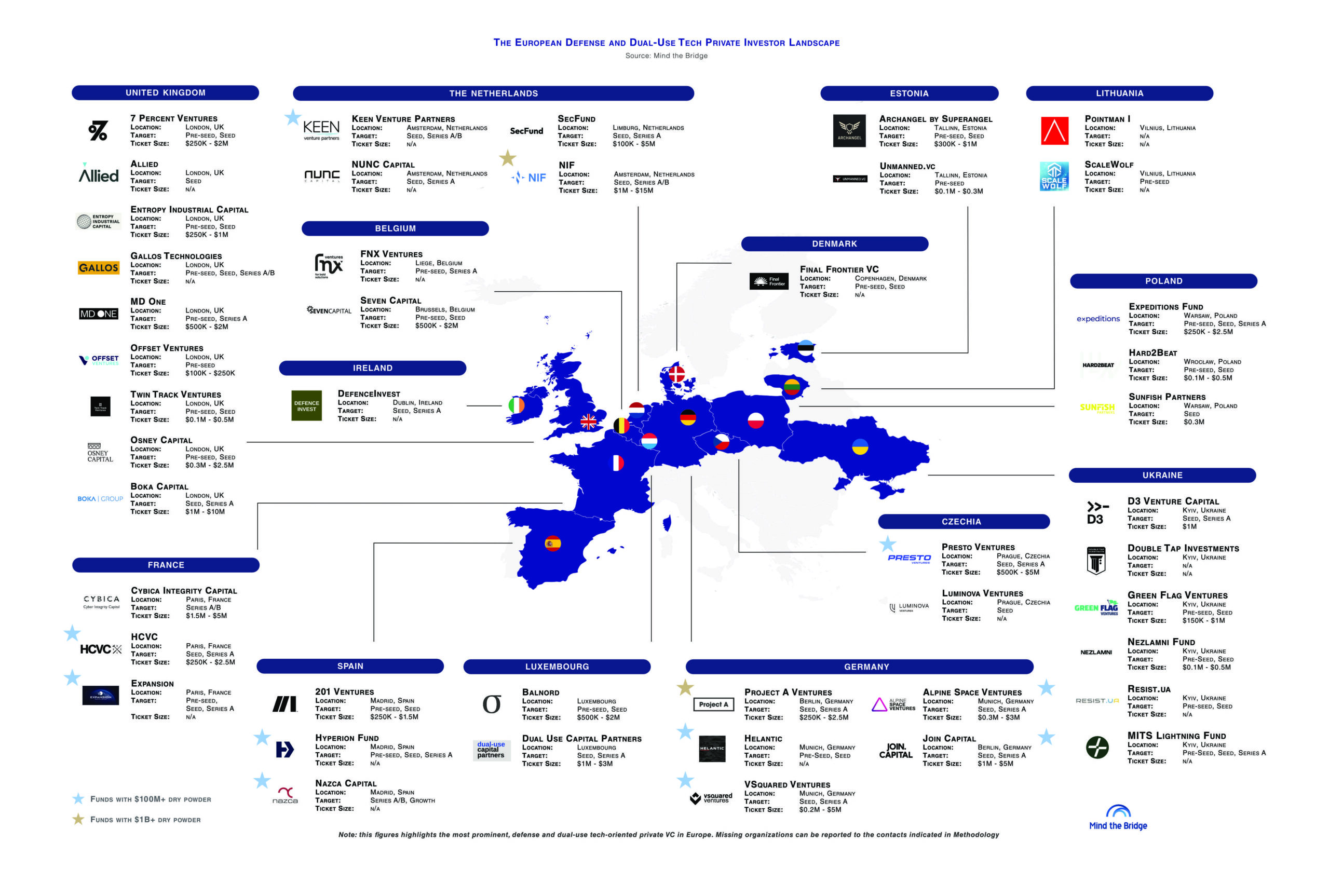

To say that, the landscape is changing. Watch out for the bridge 74 VC funds were identified around the world, which actively invest in startups with double use. Over a third (35%) is based in the United States, followed by Great Britain (12%). Another 22% are in Ukraine, Bałatyka and Eastern Europe – a sign of the growing importance of defense technology and security in these regions. (A worldwide catalog of investors energetic in double application is available Here.)