{kind=link}

The VC bubble has subsided, and last 12 months was some of the difficult years on record to boost a Series A round of funding.

As rates of interest rose and global uncertainty prevailed, the growth-at-all-costs mindset evaporated, and investors quickly began to favor startups with high revenues, capital efficiency, and high gross margins. This left many firms within the lurch 2023 will see the very best variety of startup bankruptcies in a decade.

On Kruze Consultingwe work with over 800 startups and their founders to assist them with all the pieces from bookkeeping to preparing for funding rounds and due diligence.

At the top of the 12 months, I wanted to seek out out what distinguishes the seed-funded startups that were in a position to raise Series A with colleagues who exited in 2023.

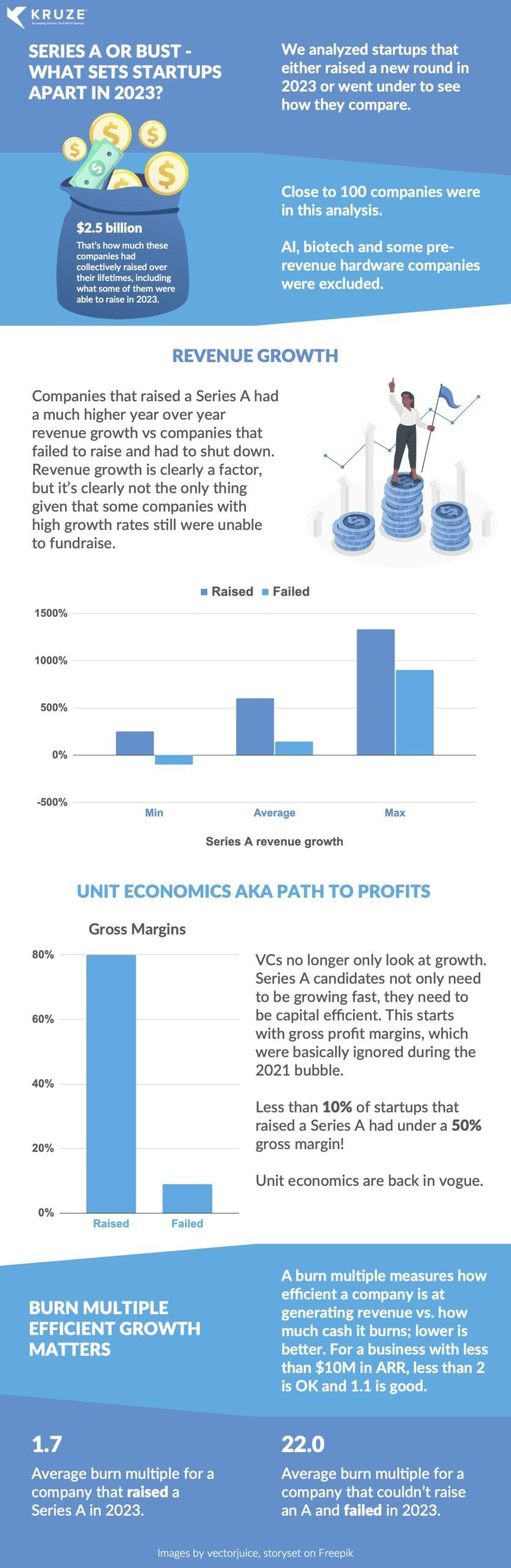

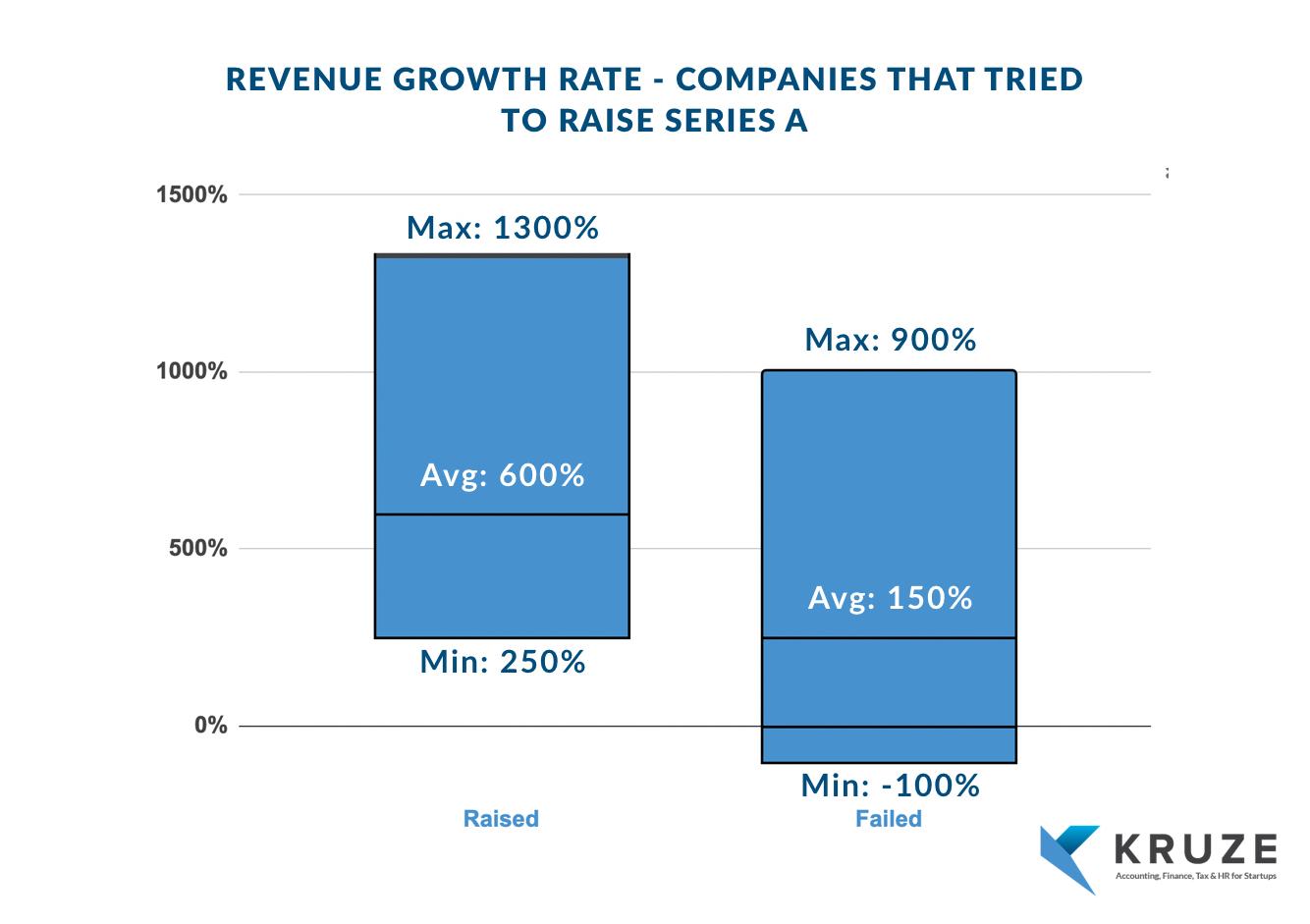

The evaluation I’m about to share looks at data from about 100 seed-funded startups that were trying to boost a Series A in 2023, comparing those who succeeded with those who failed after which went bust.

AI startups, biotech startups, and the like were faraway from the evaluation. The results reflect the shift in sentiment that the ecosystem has experienced over the past 12 months and needs to be viewed as the brand new normal for founders.

So what were the important thing indicators differentiating these two groups?

Revenue growth still matters

Revenue growth is, as at all times, a transparent signal. All firms that managed to boost funds increased their revenues on average 4 times faster than those who closed their operations. However, there have been many startups that saw impressive revenue growth that were still unable to boost Series A.

Investors value greater than revenue growth

To this end, the gross margin on these revenues provided one other clear distinction between firms that achieved growth and firms that failed. About 90% of startups raising a Series A in 2023 had over 50% gross margin, with the typical of successful firms being 80%.

Once again, the “growth at all costs” approach faded into the background as investors only invested capital in firms that generated high revenue growth.

Strong unit economics at the highest also translated to the underside line: firms that closed Series A showed a median burn multiple of just over 3x, while firms that failed were 10x worse. Only founders with capital efficiency on the helm were in a position to close one other round.

The past 12 months has been stuffed with hard-won lessons for founders and resetting the norm for venture-backed startups. Everything happened in a short time and lots of firms that didn’t have these metrics on the core of their business from the start were unable to show the battleship around in time.